Navigating Mortgage Enforcement in Ontario: Four key steps from Default to Eviction

When a borrower defaults on a mortgage in Ontario and the mortgage/charge has been registered against real property, a secured lender must act quickly to protect their investment. While foreclosure is an option, the vast majority of institutional and private lenders utilize the Power of Sale process because it is significantly faster and allows the lender to recover their capital without taking permanent title to the property.

Understanding the rigorous legal timeline from the initial default to the execution of a Writ of Possession is essential for realtors, mortgage brokers, and lenders alike. Managing these timelines, including the accumulation of interest and other costs becomes paramount when the market is in a downward cycle of depreciation or stagnation, when property values are not increasing as expected.

The four steps to mortgage enforcement are described below.

STEP 1: The Event of Default and Demand Letter

The enforcement process is triggered the moment a borrower breaches the mortgage covenants. While a default usually involves missed principal and interest payments, it can also stem from a failure to pay property taxes, maintain home insurance, or keep the property in good repair.

Before launching formal statutory proceedings, lenders typically have their legal counsel issue a Demand Letter. This gives the borrower a brief window (often 10 to 15 days) to cure the default, failing which the full balance of the mortgage is accelerated and becomes due immediately.

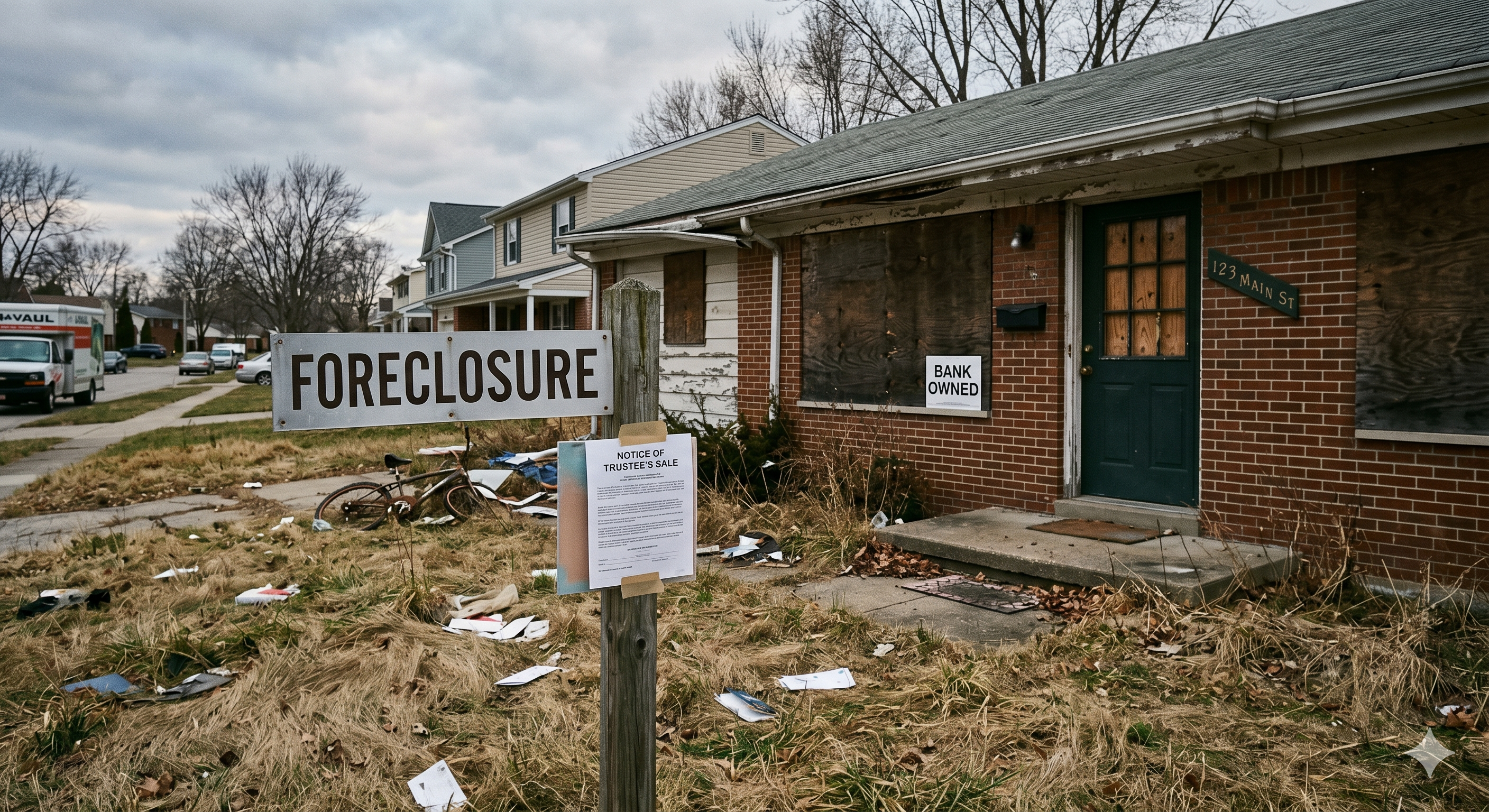

Step 2: Issuing the Notice of Sale

If the default remains uncured, the lender can issue a Notice of Sale Under Mortgage pursuant to the Mortgages Act.

-

The Waiting Period: By law, the lender cannot issue this notice until the default has continued for at least 15 days.

-

The Redemption Period: Once the notice is officially served on the borrower and all subsequent encumbrancers (such as secondary lenders or lien holders), a mandatory 35-day redemption period begins. During these 35 days, the lender cannot take further legal action, giving the borrower a statutory right to pay off the arrears or refinance. A borrower can stop the mortgage enforcement process by paying the outstanding mortgage arrears plus the lender’s reasonable legal costs to reinstate the mortgage.

Step 3: Legal Action & Court Judgment (Variable Timeline)

-

Pursuing a Claim: If the 35-day grace period expires and the default remains unpaid, the lender will pursue the amount owed by filing a lawsuit (Statement of Claim) in court. They will ask a judge for a judgment to recover the total money owed and to grant them legal possession of the property.

-

The timeline: This phase varies depending on court backlogs and whether the borrower/mortgagor files a legal defense. If undefended, a lender can typically obtain a court judgment within a few weeks to a couple of months.

Step 4: The Writ of Possession & Eviction (Final Phase)

-

Securing Possession: Once a judge grants the lender judgment for possession, the lender’s lawyer will secure a Writ of Possession from the court.

-

Enforcing Eviction: This writ is handed over to the local Court Sheriff. The Sheriff is the only authority legally allowed to enforce a physical eviction. They will deliver a notice to vacate, establish a formal eviction date, and physically attend the property to change the locks, officially delivering the vacant property to the lender.

Conclusion

As Mortgage Default rises you need expert advice to recover your investment.

There are important statutory requirements that must be strictly followed in connection with mortgage enforcement and retaining an experienced lawyer with a deep understanding of the relevant acts is critical to navigating these timelines effectively. There are strategies available that will allow a lender to expedite some of these timelines that go beyond the scope of this article. If you want to learn more about your rights and how to expedite the mortgage enforcement process call us for a free consultation.

The lawyers at Vakili Law Group have been advising individuals, development companies, real estate investment corporations, private lenders and small businesses for more than 15 years and will be happy to assist you with your matter as well. For more information feel free to schedule a free 15-minute consultation with one of our lawyers by clicking on the following calendar link: https://calendly.com/vlglaw/book-a-call-meeting